UX Case Study · Launching Afterpay on Amazon Australia

Launching Afterpay on Amazon Australia

"Amazon AU was losing high-intent shoppers to BNPL-enabled competitors"

Australia is one of the world's most BNPL-mature markets. Over 63% of Australians used BNPL products in the past year — the highest adoption rate globally. Without Afterpay on Amazon AU, the platform had a structural disadvantage against local retailers like Catch, Kogan, and JB Hi-Fi.

The absence of instalment options created silent checkout abandonment for products above AU$75, where BNPL psychology most significantly drives purchase decisions. Customers would discover on Amazon, then complete purchases elsewhere.

Amazon was also missing Afterpay's existing shopper network — a direct acquisition channel for 150,000 customers who were Afterpay-loyal but not yet Amazon shoppers.

Launching Afterpay on Amazon addresses a critical SIC BNPL parity gap and targets to drive instalment penetration lift of 6%, USD $82.9M GMS, 150K New-to-Amazon customers, with ACV of $75 (+2.1x vs AU Stores ACV $35) by YE'25.

— Project brief, Amazon AU BNPL Initiative

Opportunity

Afterpay's integration into Amazon Australia was the first time a major Buy Now Pay Later provider was surfaced across an Amazon marketplace at scale. As the lead designer, I owned the experience across every touchpoint — from how the option appeared in search results through to the post-purchase confirmation state.

BNPL is not just a payment method — it's a decision driver that enables affordability framing (e.g., '$50/month' vs. $200 upfront), attracts price-sensitive and younger users who may not have access to credit cards, and acts as a customer acquisition lever through the Afterpay ecosystem. When surfaced early and contextually, it can significantly improve conversion, increase AOV, and bring new users to Amazon.

Making Installment Payments Discoverable Earlier in the Shopping Journey

Despite Afterpay being a recognised brand in Australia, customers shopping on Amazon AU had no visibility of flexible payment options until the final checkout step — long after purchase intent had formed. The option was buried below the fold in a generic "Other payment methods" list that most users never reached.

- No Afterpay signal on search results pages

- Eligible products indistinguishable from ineligible ones

- Price-sensitive shoppers had no filter anchor

- No indication of installment availability or Afterpay eligibility

- Missed opportunity to influence decision-making at a critical stage

- Afterpay introduced late alongside 8+ other options

- Low trust due to no prior conditioning in the journey

- Customers without prior Afterpay experience skipped it

Design Approach

The strategy was progressive disclosure — introducing Afterpay at low-stakes moments earlier in the journey so that by the time a customer reached checkout, the option was already familiar and trusted.

From research to a compliant, brand-consistent integration

The process ran across five phases, with Afterpay and Amazon AU stakeholders engaged throughout.

Cross-functional kickoff with Amazon AU product, payments, legal, and Afterpay partner team. Defined success metrics, brand constraints, and design decision framework. Created a shared Figma workspace for async stakeholder review.

Mapped the full customer journey across Search, PDP, and Checkout. Identified 14 touchpoints where Afterpay could appear and prioritised highest-impact placements using a signal/noise framework.

Designed multiple layout concepts for PDP instalment messaging — testing badge placement, copy variants, and progressive disclosure patterns. Rapid async reviews with Afterpay brand and Amazon legal teams.

Multiple rounds of formal design review with Afterpay AU compliance and brand and legal teams. Resolved friction around logo, card art, legal disclosure placement, and eligibility messaging. Delivered a final approved prototype.

Produced comprehensive Figma specs and annotated handoff docs. Collaborated with Tec on QA for edge cases — ineligible products, cart thresholds, failed Afterpay auth. Obtained final sign-off from both teams and PXBR.

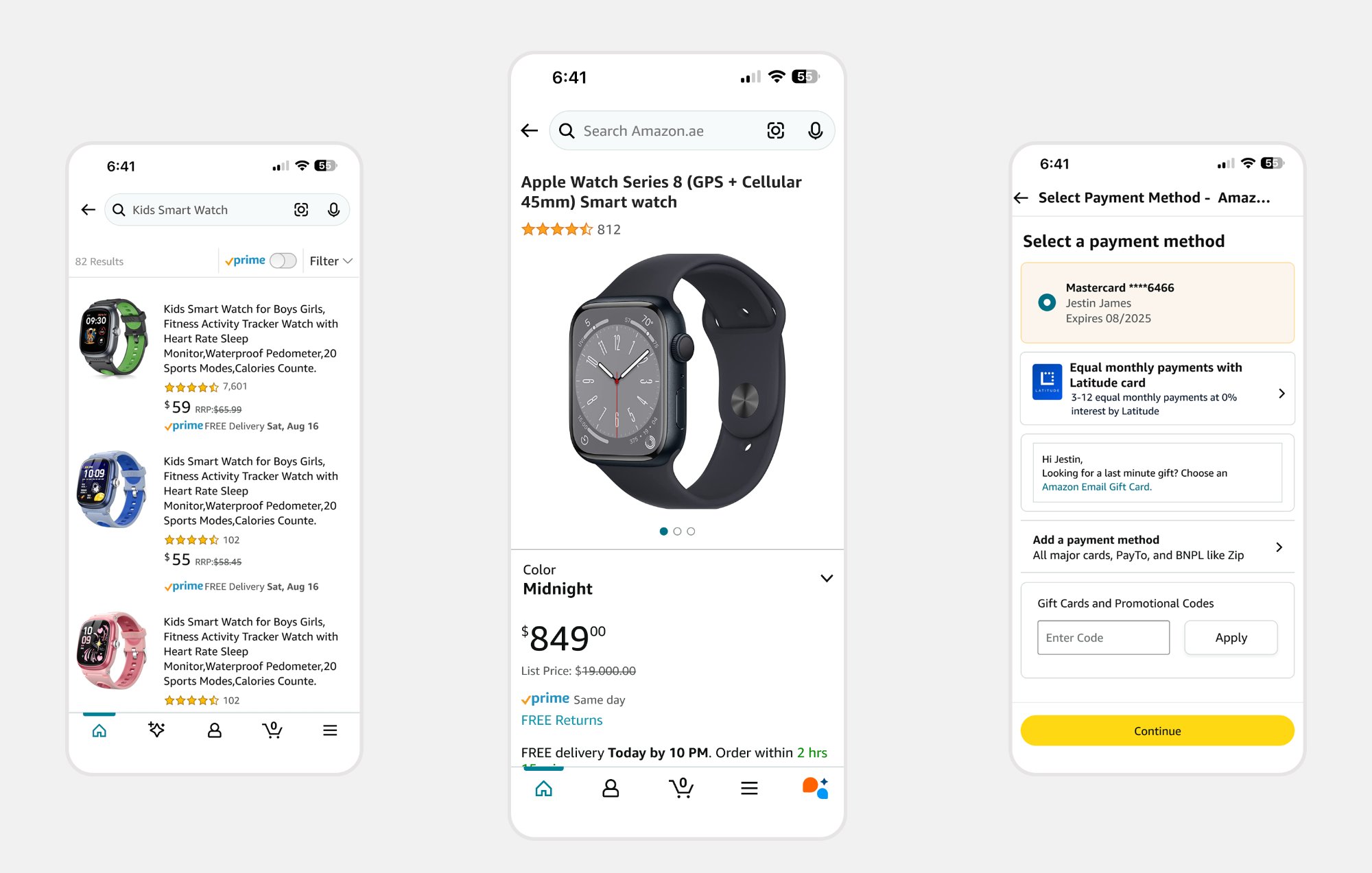

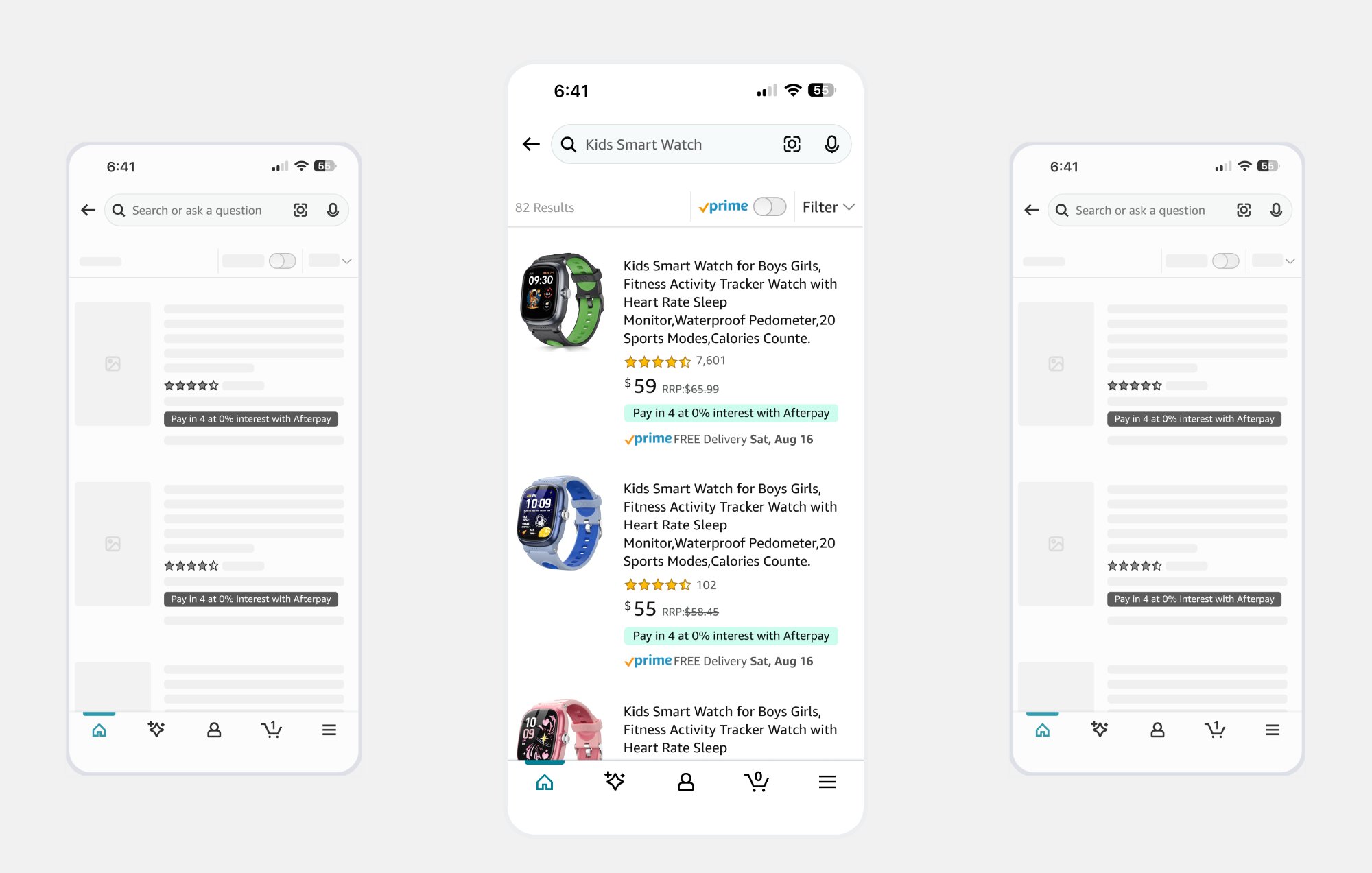

Afterpay Signals on Search Results

Designed BNPL eligibility signals for the Search Results Page on Amazon Australia to surface financing options earlier in the shopping journey, addressing the gap where users were unaware of installment options until late stages like PDP or checkout. By introducing contextual messaging such as monthly payment breakdowns and provider visibility directly alongside product prices, the experience shifted user perception from total cost to affordability, reduced price-based drop-offs, and improved engagement and conversion for higher-value items — turning payments into a discovery driver rather than just a transaction step.

- Badge appears only on products confirmed eligible — no false signals

- Positioned between the price and ratings line — the most scanned zone in eye-tracking studies

- Uses Afterpay's brand mint with sufficient contrast, rendered as a small inline chip

- On ineligible products, the row collapses — no empty space or placeholder gap

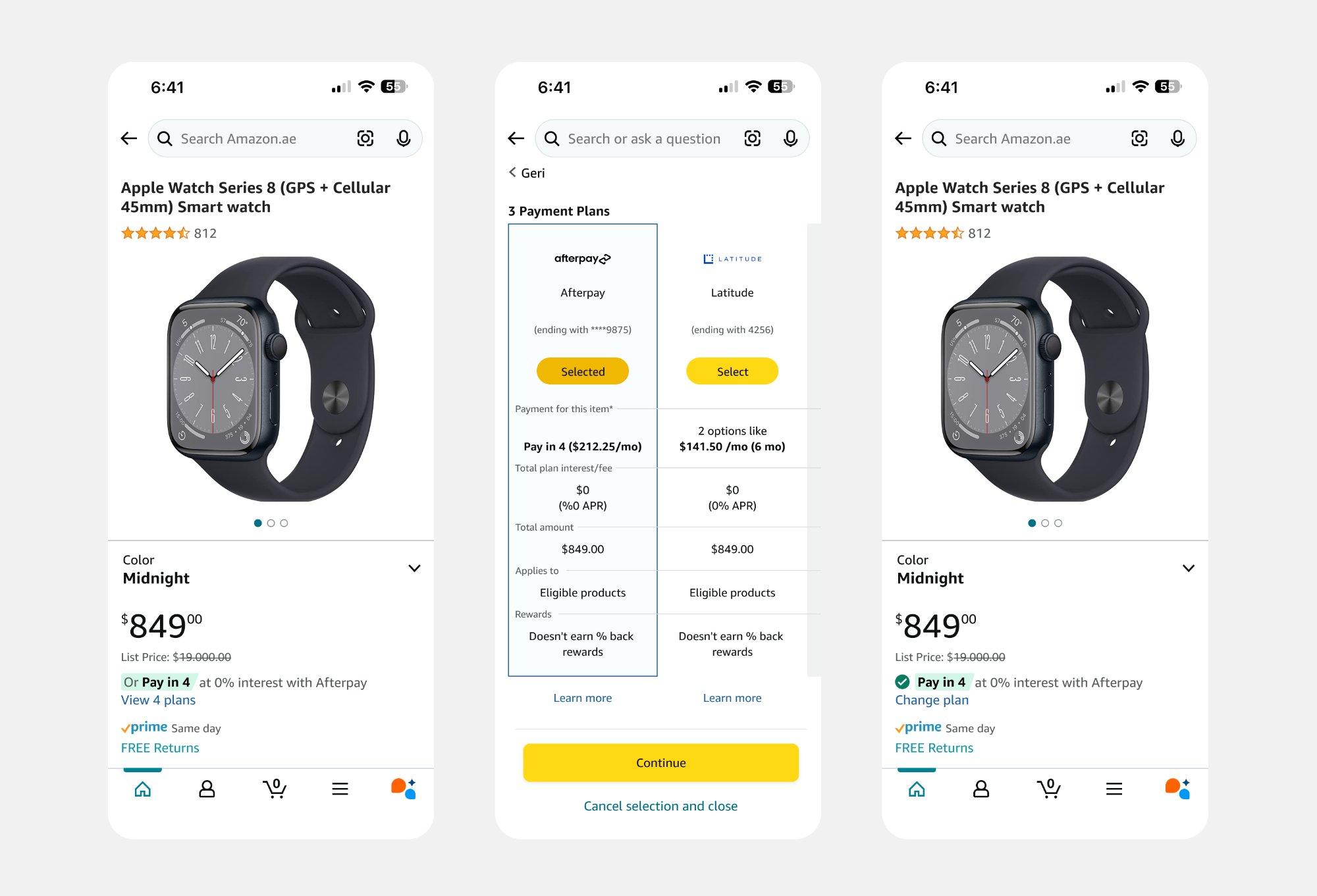

Product Detail Page — BNPL Discoverability

The Product Detail Page was the highest-impact touchpoint. Getting it right meant inserting the Afterpay signal at the exact zone where customers make the go / no-go purchase decision — without disrupting the primary CTA.

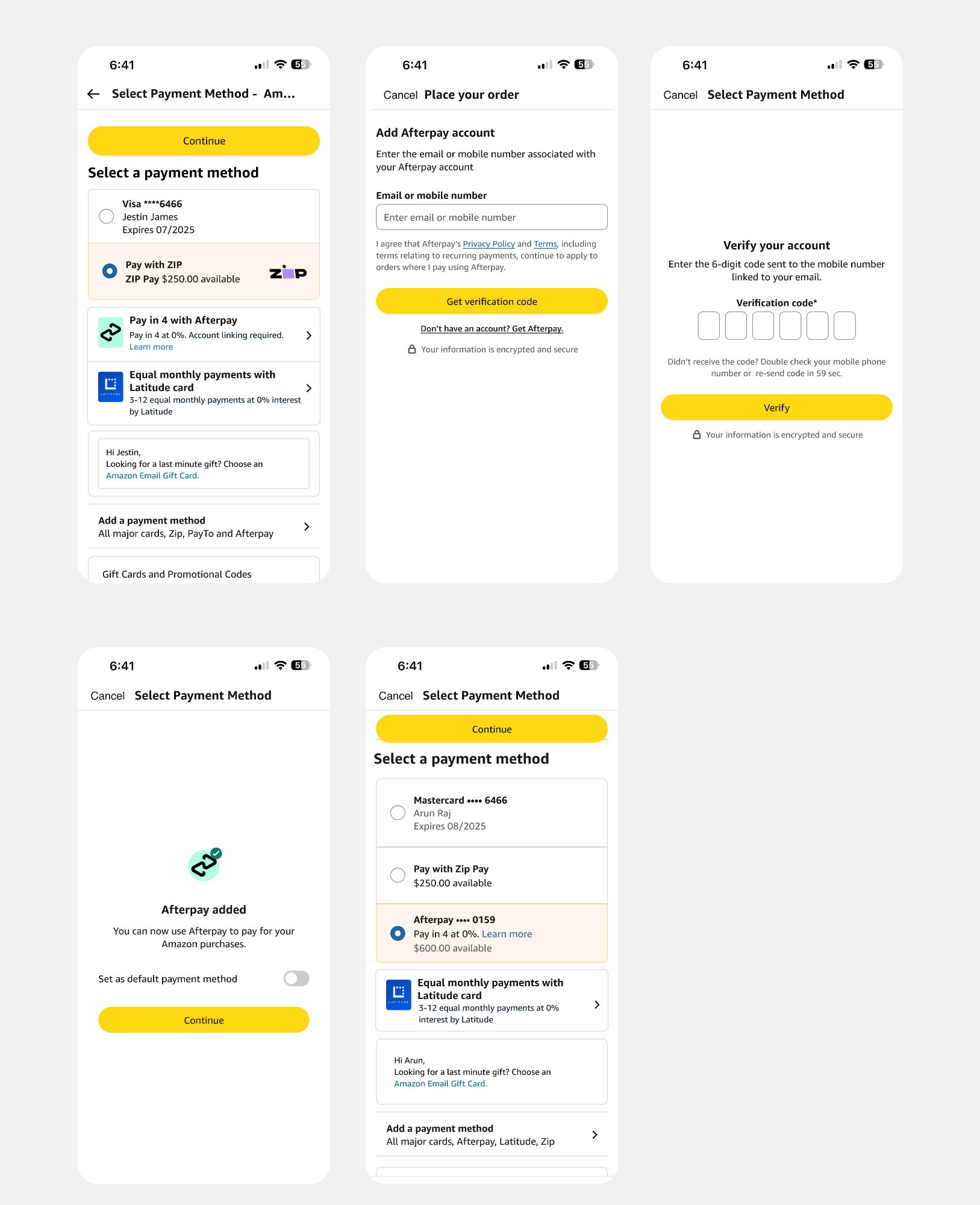

Checkout — Payment Selection

Frictionless Afterpay account linking via OTP

A key challenge in the Afterpay integration was connecting a customer's existing Afterpay account to their Amazon account at checkout — without disrupting purchase momentum. The design goal was to make linking feel fast, trusted, and low-effort. The solution: a simple OTP (one-time passcode) flow that completes in under 60 seconds with no app switching required.

Chose OTP over a full password sign-in to eliminate the most common drop-off point — forgotten passwords. A 6-digit code via SMS or email leverages existing phone habits and feels lighter at checkout.

The entire linking flow happens inline within the Amazon checkout — no redirect to the Afterpay app or website. This was a deliberate decision to preserve checkout momentum and reduce the risk of session abandonment.

Once linked, the Afterpay account persists on the customer's Amazon account. Repeat purchasers see Afterpay as a saved payment method — no re-linking, no friction. This was critical for driving repeat instalment usage beyond the first transaction.

Designed explicit error states for expired codes, invalid codes, and unrecognised email addresses — each with a clear action to recover. Preventing dead-ends at this stage was essential given the high-intent moment of active checkout.

BNPL Surfacing — Launch on Amazon AU

Following A/B testing across three cohorts, the solution launched across the full Amazon AU marketplace in Q2 2024. All three touchpoints shipped simultaneously to ensure a consistent customer experience regardless of entry point.

Business outcomes tied to design decisions

Each metric below is directly tied to a specific UX decision made during the project.

Afterpay-attributed orders targeted at 2.1x the AU Stores ACV. The PDP instalment badge reduced hesitation on high-value items by making the total cost feel manageable at the point of consideration.

BNPL reduces purchase friction, especially for mid-to-high value items

Customers tend to spend more when payments are split into installments

Surfacing instalment cost at PDP — before checkout — addressed the core drop-off pattern from AU market research. Customers who saw the breakdown early were less likely to abandon at payment.

Afterpay attracts younger, credit-averse users (Gen Z & Millennials)